Surf on Chart: Training RL model for coin trading

Agents were trained to perform coin trading using reinforcement learning

algorithms such as DQN, DDQN, A2C, PPO.

Tensorforce

library was used to implement the agents, and multiple tests were

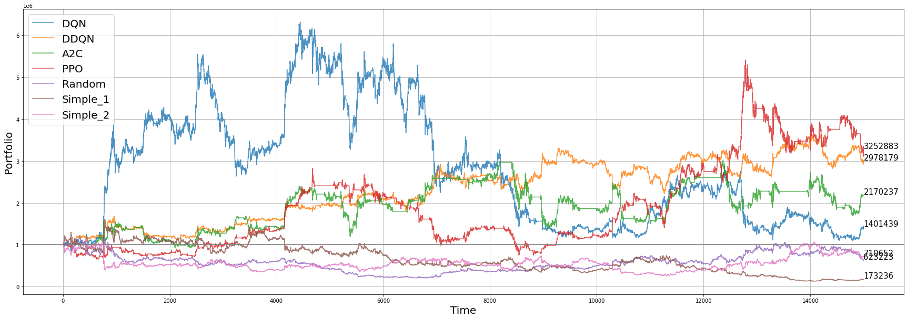

conducted to find optimal tuning parameters. In our experiments, the PPO

agent was revealed to generate the highest profit. However, due to the

high frequency of learning results falling into local optima, they

cannot be fully trusted.

RL Agents

-

A2C: A2C is a kind of Actor-Critic method which utilizes

expected output as advantage. Advantage is a subtraction of state

value from state-action value. Critic learns from advantage. A2C is

good for learning how much it will gian "more" not only the absolute

gain the agent gets.

-

PPO: PPO is a learning technique that simplifies the complex

computations of TRPO (Trust Region Policy Optimization), a type of

A2C, while maintaining its performance. During the update process, it

is limited to update only in the trusted region through clipping,

enabling more stable learning.

-

PPO: PPO is a learning technique that simplifies the complex

computations of TRPO (Trust Region Policy Optimization), a type of

A2C, while maintaining its performance. During the update process, it

is limited to update only in the trusted region through clipping,

enabling more stable learning.

-

DQN: Deep Q-Network. This method use a deep neural network in

Q-Learning, an off-policy control method of TD. The Q function is

updated using the largest Q value at the next state s'. While

selecting the action with the highest Q value, sufficient exploration

is also performed.

-

DDQN: Double Deep Q-Network. DDQN updates DQN based on the

Q-value obtained from the Target Network, which updates the estimated

Q-value for the chosen action.

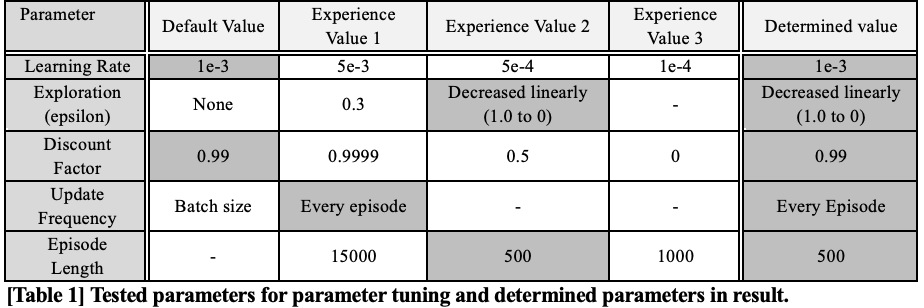

Parameter Tuning

Repetitive experiments were done for hyperparameter tuning. The default

value was set according to documentation of tensorforce library, which

we used to implement RL algorithms. We tested if bigger or smaller

hyperparameters would be better than the default value of them.

Additionally, hyperparameter values of reference papers were also

tested. The test range was narrowed in direction of some values which

showed better performance compared to default values.

Problem of model constantly choosing same action "Hold"

An endemic problem of AI investment had been reported from previous

stock and coin trading model researchers, which is that as the model get

trained more, they tend to keep selecting action “Hold”. When agent

performs action “Hold”, They do not buy or sell any assets. We observed

same problem in our own research.

The problem is that buying nor selling coin would not preserve the

initial balance in real world. The reason is that value of cash

continues to decline. We reflected the reality to our trader

environment, giving penalty to value of cash as timestep goes by. The

models trained in revised environment chose “Hold” less. Additionally,

we introduced idea of “Long” and “Short” positions to our environment so

that agents could be capable for much more aggressive investment. This

also reduced the problematic situation that trained models only tend to

“Hold”.

Tuning episode length for best performance

At the beginning of experiments, whole chart data (Bitcoin

open/close/high/low/volume data from 2017-12-09 23:00:00 to 2018-02-03

12:15:00 with 5-min timestep) was used, counting up to 15000 tick data.

However, in this case, loss did not decrease stably, thus model was not

trained appropriately. In order to resolve the problem, we conducted a

little research and referenced Github community of Tensorforce library.

A researcher who was struggling on same problem (which means model

seemed to be not learning) reported the problem to the Github community,

and Tensorforce developers explained that too long training episode

might be troublesome for training and recommended to lessen the training

data.

According to the idea we used shorter episode length and reconducted

experiments. 3 different piece of chart data with length 500 tick was

used as training data. Initially, we programmed the trainer code to get

random 3 slices. However, because we aimed to train agent with different

RL algorithms and compare them, we had to eliminate the randomness and

fix the training slices. Bull market, bear market, and box patterned

market were selected as training data because trained model should make

a profit at any environment after the training phase. Bull market

specifies a market which has continuously rising coin price, bear market

represents a market with continuously falling coin price, and box

patterned market means a market which has both price falling and rising

phase, but not showing outstanding falling nor rising.